[ad_1]

There are plenty of billion-dollar-plus sensor businesses already. The top 15 sensor manufacturers have $45 billion in such activity if we include the value of sensors they manufacture for use in their own products. What next? The New Zhar Research report, “Sensor Materials and Systems Markets 2023-2043” has the detail. It takes its cues from specific patent trends, the latest research pipeline, the future of the user industries, insider viewpoints and more. It finds some trouble ahead, limiting overall growth to 3% CAGR with some declining sectors but others growing very rapidly, so careful selection will be essential.

For example, automotive and energy have been large markets for sensors but electrification reduces parts by up to 99% and fuel supply chains vanish, eliminating sensors from mine to burner. Well within 20 years, sensors for the fossil-fuel heritage will be circling the drain. This will be despite latest forecasts by the EIA and S&P predicting oil and gas sales holding up on what Shakespeare called, “the primrose way to the everlasting bonfire”.

Fastest growing sectors

Zhar Research sees most other sectors growing faster and telecommunications sensors – including those incorporated into client devices such as Internet of Things nodes – eventually becoming the largest sensor market sector by value. Overall, in 2043, expect a massive $232 billion business just for sensor hardware.

Electromagnetic wins

Cutting it by technology, electromagnetic sensing will lead at $52 billion. It will involve microwave, terahertz/ far-infrared, near-infrared, visible and ultraviolet sensing that determines magnitude, change, spectrum analysis or imaging. There will also be use of electromagnetic radiation to monitor temperature, distance and so on.

However, care is needed. For example, the largest potential market for LIDAR sensors was supposed to become automotive but market leader Tesla does not use them. No ultrasound either. Recently, several major car manufacturers, loaded with debt, have dropped their autonomous vehicle programs, LIDAR included.

Large new markets

The twenty-year viewpoint is essential to capture the large new markets being created. They include such things as new heavy industry in the form of long-duration grid storage (liquid air, compressed air etc.) and 6G Communications which includes that new terahertz market.

Zhar Research has a close look at design trends and the research pipeline but also industry dynamics to form its predictions. For example, smartphone sales dropped 12% last year and an increasingly global recession will not help them rise again. On the bright side, 6G Communications will later transform the capability and desirability of smartphones and other client devices. In a multiplier of growth, the number of sensors in a smartphone, smart watch and so on will double. 6G will particularly boost sensor sales in its Phase 2 around 2035 when it becomes largely optical and also enables vast numbers of battery-less client devices full of sensors – or such is the intention. See Zhar Research report, “6G Communications: Optical Materials and Components Markets: Visible, Near IR, Far IR from 0.3THz 2023-2043“.

Needs to be avoided and those to prioritise

Those hoping to create a billion-dollar sensor business from yesterday’s sectors will be disappointed. They include coal, oil and gas fuel and vehicles and generators using fossil fuels. That is despite some initial growth. Better to address such sectors as bionic man and woman, the expected 500 million with diabetes, unmanned factories, mines and aircraft, even robot ships and unmanned farming.

Nuanced opportunities

Dr Peter Harrop CEO of Zhar Research adds,

“There are also more nuanced opportunities from such things as multifunctional sensors and more sensor fusion where software makes several sensors greater than the sum of the parts. This is biomimetics mimicking how your body works. It will include smart skin as structural electronics performing more than just sensing. Some sensing business will transmute into smart material feedstock.”

He adds,

“Then there is the vision of an Internet of Senses based on devices, sensors, actuators and context-aware applications. It is intended to make our digital experiences richer, involving all our senses, and ultimately merging the digital and the physical worlds – or so they say. How much actual business that creates over the next twenty years remains to be seen. ”

Technology excellence ahead

Certainly, in planning your next billion-dollar sensor business you would do well to track leading technology trends such as miniaturised and integrated sensors, selling the associated software and systems as well. For instance, startup Senbiosys utilizes six photoplethysmogram (PPG) sensors in its new smart ring plus 18 microLEDs which provide the returned light they utilise. When paired with an accompanying smartphone app, data gathered by the ring’s PPGs, thermometer and accelerometer are used to determine the wearer’s heart rate, respiration rate, step count, body temperature, blood oxygen level, sleep quality, stress level and calories burned. Another new example is MIT MechSense. This is showing the way by 3D printing of wireless sensors directly into rotating parts.

Learn from the best

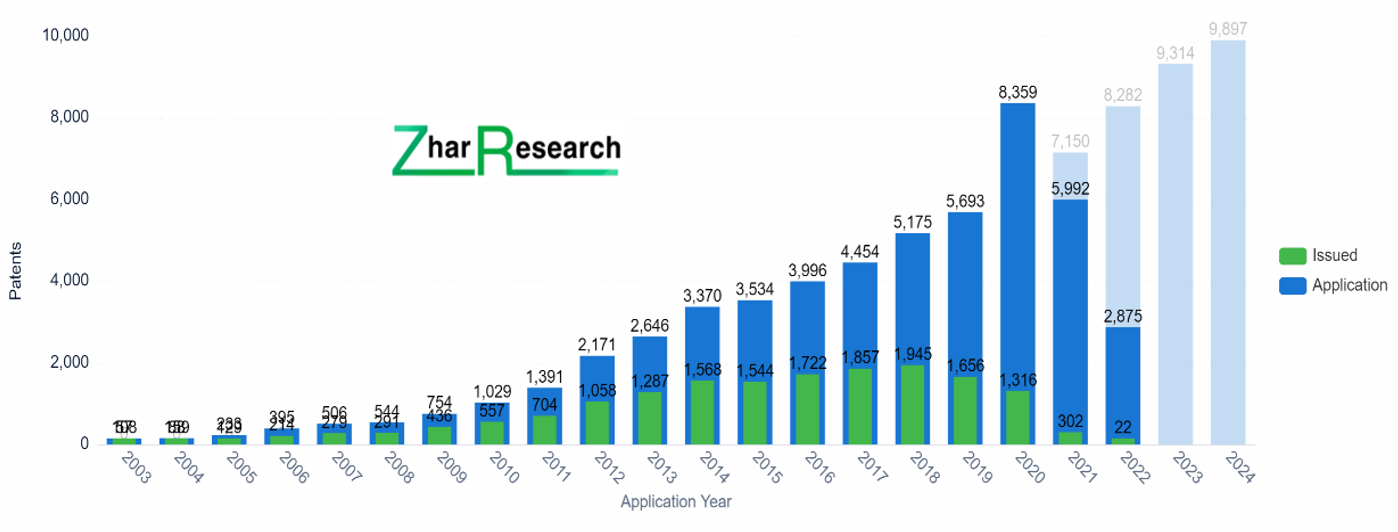

Many emerging sensor manufacturers are identified in the new report. Some have formidable innovation in the best sectors but no in-house sales. Consider them as possible acquisitions, sources or partners. Learn from existing well-run sensor businesses such as $3.8 billion Sensata Technologies (strapline “sensing is what we do”) and TE Connectivity. For example, TE will rise with its choice of aerospace, military, industrial, medical and air-conditioning sensor systems boosted by global warming by the fact that emerging economies are mostly in tropical regions. Sensata focus wisely includes sensors for the electrification of vehicles and the power grid. They succeed without being top patentors of sensors, though patenting remains important. Heavy sensor patentor Sony shrewdly prioritises sensors for electric vehicles, robotics, personal electronics and, like Sensata, deliberately prioritising very advanced sensor technologies. Teledyne is also very much up-market in its billion dollar sensor activity.

Lessons of poor positioning

Set against this, Zhar Research identifies some top patentors that are not in a strong position for the future because they are too reliant on imperilled market sectors, having earnings, profits or patenting trending down and failing to lead competition in sensor technology or use.

Big picture essential

The report is unusual in looking at the whole sensor business because your opportunities may be wider than you think. It closely covers companies selling to themselves and selling custom sensors because the catalog sensor business is only the tip of the iceberg. The booming business in image sensors is a strong example of in-house and custom uses.

League table for the future

The Zhar Research supplier league tables are based on forward-looking criteria such as sensor patenting amount and trend, focus on growth sensors markets, innovation, sales and in-house use. Zhar Research rates Samsung top sensor company for 2023-2043 on current evidence. It makes the Tesla embedded cameras and the sensors for its smartphones that outsell everyone but it is also expanding in medical sensing and more. However, sensor-outsiders Apple and Qualcomm now patenting sensors like there is no tomorrow. Qualcomm newly offers a Snapdragon Digital Chassis as the heart of sensors and most else in electric vehicles. For more see Zhar Research report, “Sensor Materials and Systems Markets 2023-2043“.

[ad_2]

Source link